Baby-boomers are starting to retire. They expect to receive Social Security since most of them have contributed to the program all of their lives. They expect to receive Medicare benefits, because private insurers have been virtually driven from the retiree market. These two programs alone constitute about a third of the current US budget.

However, Social Security is already running a deficit, creating more inflation as government spends money it does not have. The check seniors receive buys less and less each month, essentially gutting the promised benefit.

As our population grays, we have fewer workers than we did in the past supporting each retiree. In 1950, approximately 16 workers paid the Social Security checks of each retiree; today, fewer than 3 workers do so. Social Security taxes must be raised dramatically to make the system solvent, making it harder for the younger generation to get ahead.

What of Medicare? Obama has already slashed its budget and more cuts may be coming. Many doctors are deciding that the red tape, delayed payments, and slashed fees just aren’t worth it. My physician, along with many others, have already sent notices to those who are approaching senior status that they won’t be taking Medicare. The “free” health care program that seniors have paid for all their working life might be theirs in theory, but in practice they are likely to die waiting in the same long lines that Canadians and Brits have to deal with. Raising taxes enough on workers to alleviate this wait will burden the retirees’ children and grandchildren further. Deficit spending creates more inflation, shrinking retirees’ Social Security checks and essentially having them pay for the “free” health care program that they’ve been taxed for throughout their working career.

Are these our onlychoices? Should we deficit spend and create the subsequent inflation which shifts the burden to seniors who have paid into these programs all of their lives? Should we raise taxes and make the next generation pay about 5 times more for retiree Social Security than their parents and grandparents did? Instead of choosing between these two heart-rending choices, libertarians have a win-win solution to offer that has been validated in the most stringent testing ground of all—the real world.

The problem with more taxes or deficit spending is that jobs are destroyed and their productivity is lost. The country, as a whole, has less wealth, not more. Redistribution kills the goose that lays the golden egg. Why not nurture the goose and enjoy a lot more golden eggs?

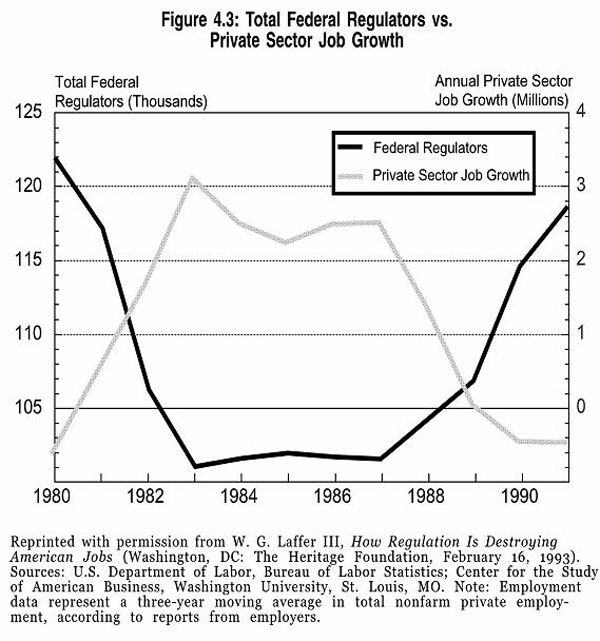

Nurturing the goose, or in this case the economy, means slashing the regulation that stifles it and using the savings to lower taxes. Figure 4.3 from my book, Healing Our World, illustrates how each federal regulator kills about 150 private sector jobs a year and how these jobs were recreated in the 1980s when the number of regulators was slashed.

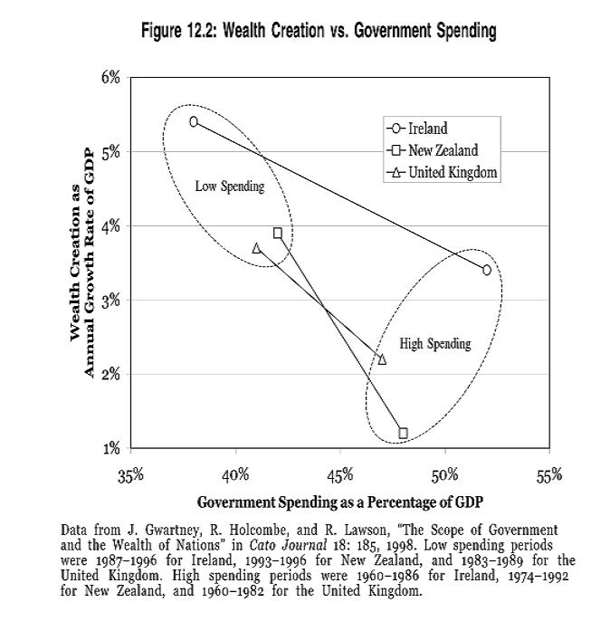

More jobs—and less government spending on regulation—mean more wealth creation. Countries that made these reforms, as illustrated in Figure 12.2 of Healing, enjoyed a dramatic and rapid increase in their Gross Domestic Product or GDP, a measure of wealth creation or “golden eggs.” When regulations stopped hampering productivity, private sector jobs skyrocketed.

If you are new to my blog or libertarianism, you may be wondering “Won’t deregulating mean that consumers are harmed?” The short answer is a resounding “No!” but you can get more detail by reading my posts on “Consumer Protection: The Compassion that Kills” or Chapters 4-10 in the 1993 version of Healing Our World in the Free Library. You’ll discover that the jobs created by deregulation end up employing the disadvantaged who create and enjoy most of the new wealth.

The taxes that formerly supported the regulators can be shifted to Social Security. With the creation of extra jobs by deregulation, more taxes will be collected without any increase in the tax rate because more people will be working. If it is also shifted to Social Security, rather than to new spending projects that politicians are so fond of, seniors can get the Social Security they were promised without taxing the young further or inflating through deficit spending.

What about Medicare? The health care industry is one of the most heavily regulated. From my research with the pharmaceutical industry, about 80% of what we pay at the pharmacy is the overhead caused by regulations that harm instead of help us (see the links to Deadly Secrets Behind Soaring Pharmaceutical Prices in the Free Library Resources page). Simply deregulating the drug industry would decrease health care costs by as much as 50%, since using a pill or nutrients to cure disease instead of surgery and hospitalization saves a great deal of money. For example, Tagamet, the anti-ulcer first drug, saved its users a $25,000 surgery and the lost time that accompanied it. At $1,000-$2,000, it was a health care bargain. Deadly Secrets illustrates how today’s regulatory climate keeps many life- and cost-saving interventions from ever reaching the marketplace.

Deregulating health care would likely decrease costs sufficiently that current Medicare taxes would be sufficient. Seniors would get the care they need without a long wait or burdening their children and grandchildren with the bill.

Will these reforms allow Medicare and Social Security to remain solvent? Possibly, but there will always be the temptation for politicians to re-regulate or spend the money collected for Social Security and Medicare on other things. That’s essentially what they’ve done in the past. There is no money in the so-called “trust funds” for these programs; the money has been spent on other programs and the trust fund is full of IOUs that must be collected from taxpayers to keep the programs solvent.

No one will save as carefully for your financial and medical needs after retirement as you will. Politicians have every incentive to use the money government collects to promise more give-aways to voters today instead of keeping it safe and sound for your retirement tomorrow. Unless you have direct control of your assets, your golden years may turn out to be a fiction. You may be forced to work just to insure that you can pay your bills, in spite of decades of paying into the Medicare and Social Security Ponzi-schemes.

Stimulating the economy via deregulation can help us keep our promises to seniors without bankrupting the next generation. However, to put retirement savings and elderly medical care on a firm footing, we must phase out government-controlled Social Security and Medicare so that the money that our workers set aside for retirement is actually there when they need it. Phasing these programs out and returning control of their hard-earned money to the workers is the only way to protect their savings from being used as a political football. Privatizing Social Security has increased the income of seniors in a number of other countries. Don’t our retirees deserve more too?

3 thoughts on “Can We Keep Promises to Our Seniors Without Bankrupting Our Children and Grandchildren?”